Case Studies(04)

/ CASE STUDY 01

Iris Energy

NASDAQ: IREN

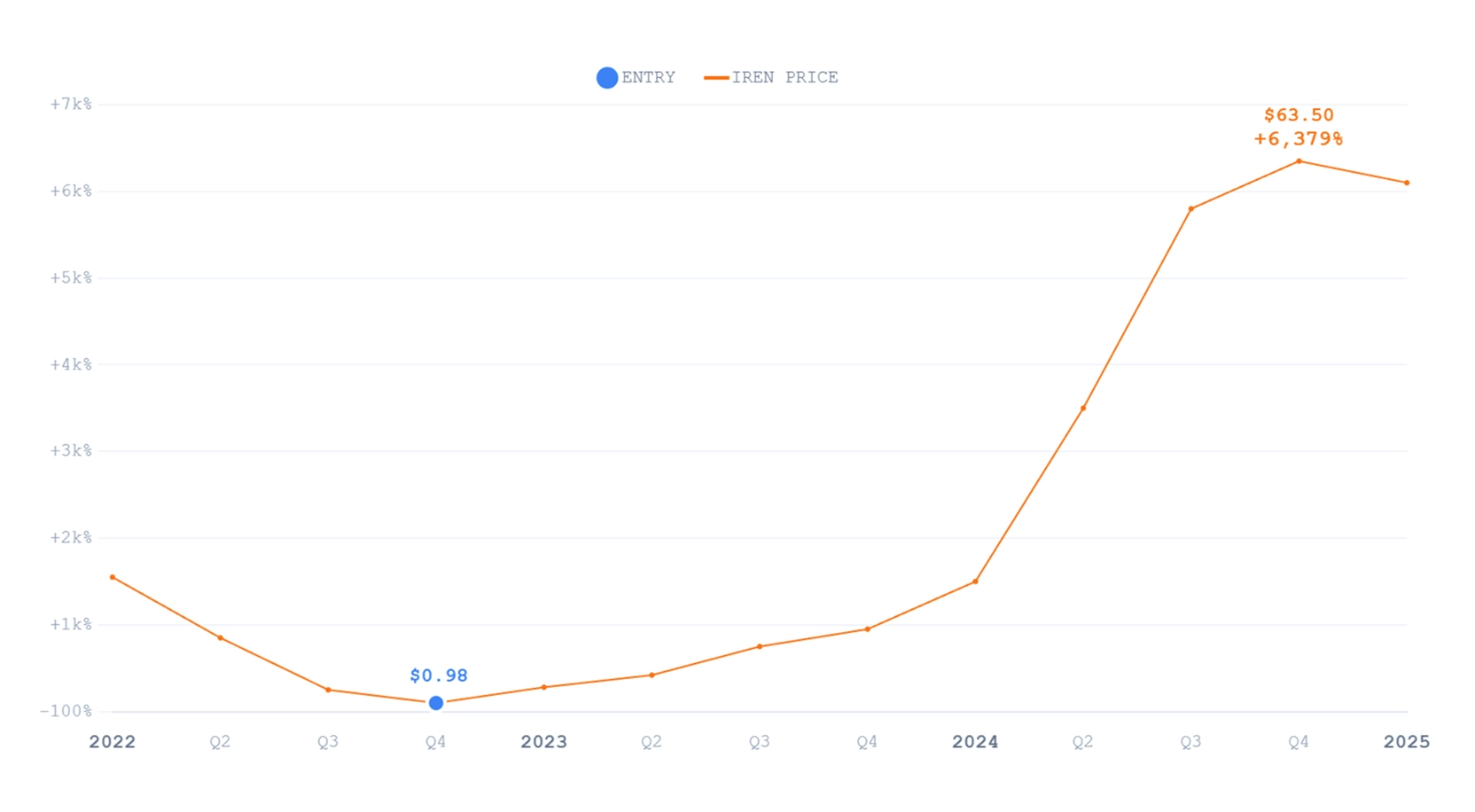

$0.98

Entry Price

> $60.00

Peak Price

Value created > $50M

Outcome

In 2022, Iris Energy sat at the intersection of two forces the market was aggressively discounting: Bitcoin mining and energy-intensive infrastructure. The prevailing narrative was simple. Miners were over-levered, power prices were rising, and capital markets were closed. Equity was treated as optional, if not expendable.

My interest in Iris Energy began not with price, but with people and assets. Through direct engagement with the founders, it became clear that this was not a financial-engineering exercise. The business was built around hard, tangible infrastructure: owned and contracted power connections, purpose-built data centre assets, and a balance sheet structured to survive prolonged stress. Unlike many peers, Iris controlled its energy destiny rather than renting it at the margin.

At the time, the market capitalisation implied that these assets were worth less than replacement cost, even before assigning value to optionality.

The original thesis rested on three pillars.

- First, asset backing. Power connections at scale are scarce, slow to replicate, and increasingly strategic. These were not speculative permits. They were real, energised assets with long useful lives.

- Second, survivability. While the market focused on Bitcoin price, the more important question was endurance. Iris was positioned to outlast the cycle without forced dilution or insolvency.

- Third, embedded optionality. Bitcoin mining was the initial use case, but not the terminal one. Any business controlling large-scale, low-cost power had latent optionality that the market was not pricing.

As Bitcoin prices fell and sentiment collapsed, the stock declined from roughly $5 per share to between $1 and $1.50. Importantly, none of the core elements of the thesis broke during this period. The assets remained. The power remained. The team remained disciplined.

This disconnect created the conditions for concentration. While the market extrapolated distress, the underlying economics were becoming more attractive. Replacement costs were rising, competitors were being flushed out, and survivability was quietly turning into strategic advantage.

The re-rating did not occur gradually.

Over an 18-month period, the market shifted from viewing Iris as a distressed Bitcoin miner to recognising it as scarce digital infrastructure with multiple potential tenants. The emergence of AI-driven compute demand acted as the forcing function, but it was not the origin of value. It merely revealed it.

What had been priced as a melting ice cube was re-rated as a long-duration asset.

The stock moved from its trough to over $60 per share in a compressed timeframe, delivering value to shareholders well in excess of $50 million. The magnitude of the outcome was a function of two things: how wrong the market had been, and how patient concentration had been allowed to compound.

The lesson was not about predicting narratives. It was about recognising mispriced infrastructure, understanding what truly mattered for survival, and having the temperament to hold when price divorced itself from reality.

/ CASE STUDY 02

Stratton Car Finance

PRIVATE EQUITY

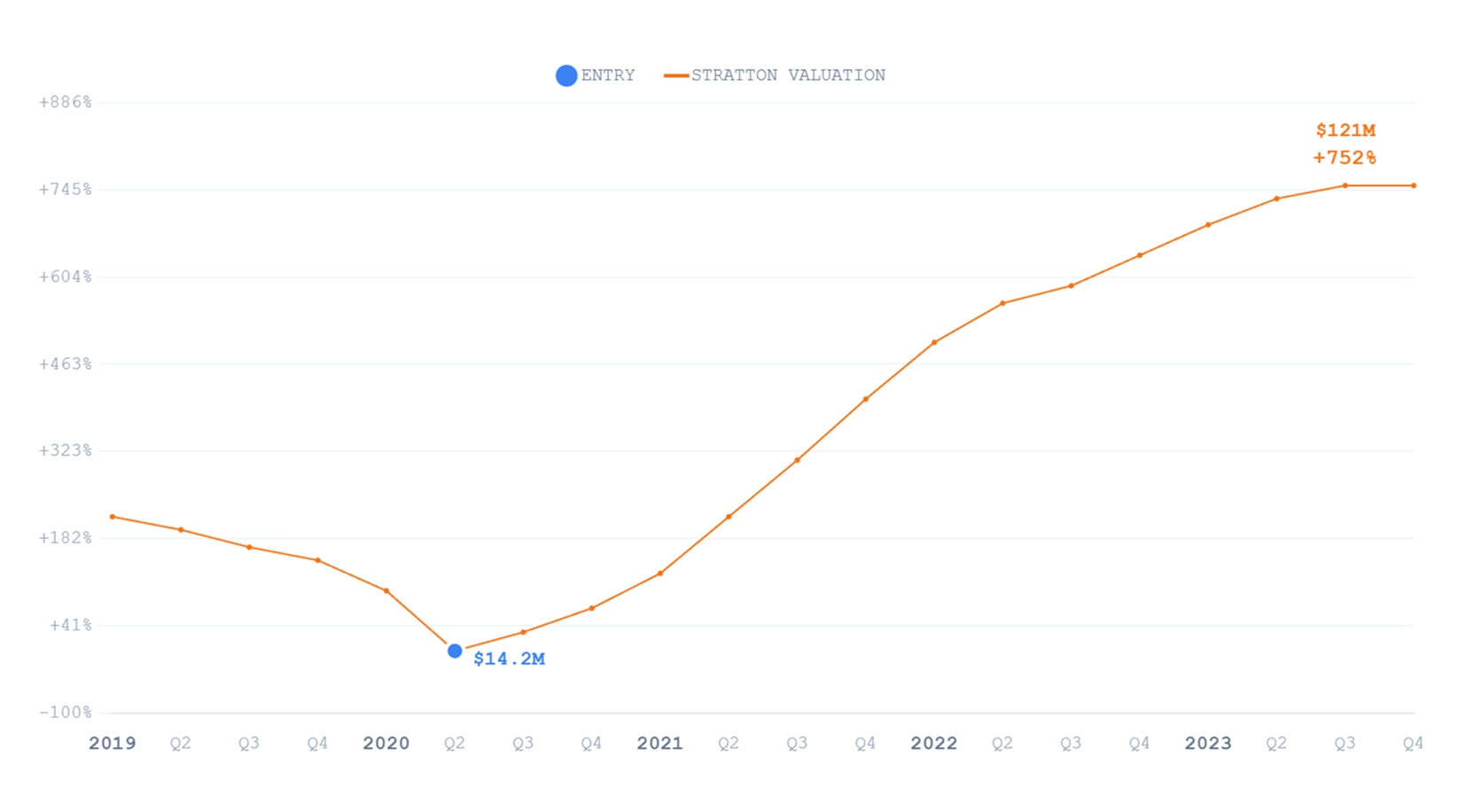

$14.2M

Entry Valuation (EV)

$121.0M

Exit Valuation (EV)

Structure over Narrative

Strategy

This investment began with familiarity, not spreadsheets. Stratton Car Finance was founded in 1998. It had operated for more than two decades. It built a dominant brand in Australian car finance.

The founder was my neighbour at the time. I saw the business up close, long before I invested. I understood its culture, reputation, and operating discipline. This mattered more than reported earnings.

The core asset was intangible. The Stratton name carried weight across dealers, lenders, and consumers. As a private business, this brand value was hard to price. In calm conditions, the market ignored it. In stressed conditions, the market wrote it off entirely.

The Dislocation

COVID created those stressed conditions. The Australian government imposed strict movement restrictions. Physical car inspections were suspended. For a car finance broker, this cut revenue at the knees.

I viewed this as policy overreach. It was emotional and temporary. It mirrored how markets behave during panics. Extreme action driven by fear, followed by eventual reversal. Stratton faced an existential shock. Revenue collapsed. Sentiment turned. The business looked broken on the surface.

I focused on what did not change. Stratton operated a capital light model: No heavy inventory. No manufacturing risk. Limited fixed costs. Strong lender relationships.

I took an outsized position. I acquired close to one third of the business. The entry valuation was an enterprise value of $14.2 million. This was not a recovery trade. It was a survival bet grounded in structure, not optimism.

The Outcome

Over the following three years, restrictions eased, dealer activity returned, and transaction volumes normalised. The brand regained relevance overnight. Nothing new was built. Nothing clever was added. The business reverted to its natural operating state.

Once conditions stabilised, strategic value became obvious again. A listed buyer acquired the business at an enterprise value of $121 million.

The outcome was a direct result of three factors: Durable brand built over decades, capital light economics that absorbed shock, and willingness to act when fear replaced judgment.

If you study this case, focus on structure over narratives. Temporary revenue impairment does not equal permanent value loss. Businesses built without financial strain survive policy mistakes longer than public patience.